Financial Planning for Young Adults in 2025: How to Clear Debt, Build an Emergency Fund, and Start Investing Smartly

Updated: April 2026 | Category: Personal Finance | Reading Time: 12-15 minutes

Featured image source: Pexels

Quick Summary: If you are young, earning, struggling with savings, worried about loans, or confused about where to invest first, this guide will help you create a realistic financial plan step by step. We will cover budgeting, debt repayment, emergency funds, smart investing, and financial habits that can change your future.

Why Financial Planning Matters More Than Ever for Young People

For many young adults, money disappears faster than it arrives. Salary comes in, bills go out, subscriptions renew, shopping happens, EMIs get deducted, and suddenly the month ends with no savings. This cycle feels normal, but it is dangerous. If you do not control your money early, your money will control your choices later.

Financial planning is not only for rich people, married couples, or people nearing retirement. It is for students starting their first job, freelancers with irregular income, young professionals living in cities, and anyone who wants peace of mind. The earlier you build smart money habits, the easier your future becomes.

Good financial planning starts with people-first, useful, trustworthy content and practical decisions, not shortcuts or fake promises. Google also recommends creating helpful, original content written for people rather than search engines, and stresses clarity, trust, strong page titles, and useful structure [Source](https://developers.google.com/search/docs/fundamentals/creating-helpful-content) [Source](https://developers.google.com/search/docs/fundamentals/seo-starter-guide).

Table of Contents

The Biggest Money Mistakes Young Adults Make

Most financial problems do not start with low income. They start with poor structure. Young earners often make the same mistakes: spending first and saving later, using credit cards for lifestyle purchases, ignoring emergency savings, taking personal loans for avoidable expenses, and investing randomly because of social media trends.

Another common mistake is trying to look financially successful instead of becoming financially stable. Expensive phones, unnecessary bike upgrades, branded fashion, weekend spending, online impulse buying, and EMI-based living can create a financial image of success while silently building stress underneath.

If you are in your 20s or early 30s, your biggest advantage is not high salary. It is time. Even small financial corrections made today can create massive long-term results.

A Real-Life Financial Planning Example

Imagine a 27-year-old working professional earning a monthly take-home income of ₹35,000. Rent, food, commuting, family support, and basic bills take away around ₹24,000. On paper, ₹11,000 should remain. But there is also a personal loan EMI of ₹4,500, a credit card due, random online spending, and no emergency savings. By the end of the month, almost nothing is left.

This is not an uncommon story. Many young people are not broke because they earn too little. They are stuck because they have no system. Once you create a system, your money starts behaving differently.

Important lesson: A salary is not a financial plan. A budget, debt strategy, emergency fund, and disciplined investing together create real financial stability.

Step 1: Build a Budget That Actually Works

A budget should not feel like punishment. It should feel like control.

Start with this basic formula:

Income - Fixed Expenses - Debt Payments - Essential Lifestyle Costs = Actual Monthly Surplus

Now divide your spending into four buckets:

- Essentials: rent, food, electricity, transport, medicines

- Financial obligations: EMI, loan repayment, insurance premiums

- Growth: savings, emergency fund, investments

- Lifestyle: eating out, entertainment, shopping, subscriptions

If you do not know where your money goes, check your last 60 days of bank statements and UPI history. You will usually find the problem quickly: food delivery, impulse purchases, frequent small spends, and payments you barely remember making.

A simple practical rule for youth is this:

- 50-60% for essentials

- 10-20% for savings and debt reduction

- 10-20% for future investing

- rest for lifestyle, only if affordable

Budgeting and cash-flow awareness are core parts of building savings and avoiding future debt traps [Source](https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/).

Step 2: Clear Debt the Smart Way

If you have debt, do not panic. But do not ignore it either.

List every debt in one place:

- loan name

- total outstanding amount

- interest rate

- minimum monthly payment

- late fee risk

Now prioritize in this order:

- Credit card debt

- High-interest personal loans

- Informal borrowing with pressure or interest

- Other structured loans

Why start with credit cards? Because credit card debt can become one of the most expensive forms of borrowing if balances are not cleared fully every month. If you only pay the minimum due, the remaining balance keeps attracting charges and traps your future income.

You can choose one of two debt payoff methods:

1. Avalanche Method

Pay the highest-interest debt first while continuing minimum payments on the rest. This saves more money in the long run.

2. Snowball Method

Pay the smallest debt first for motivation, then move to the next. This is emotionally powerful for beginners.

If you are disciplined, the avalanche method is usually stronger. If you lose motivation easily, snowball can help you stay consistent.

Step 3: Build an Emergency Fund Before Chasing Big Returns

One of the smartest moves any young adult can make is building an emergency fund. This is money kept aside only for real emergencies such as medical expenses, urgent travel, job loss, family needs, or sudden repairs.

Without emergency savings, even a small financial shock can push you into loans or credit card debt. Consumer finance guidance also explains that emergency savings help people recover faster from unexpected events and reduce dependence on debt [Source](https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/).

How much should you save?

- Starter goal: ₹10,000 to ₹25,000

- Next goal: 1 month of expenses

- Strong goal: 3 to 6 months of expenses

If that sounds too much, start very small. Even ₹50, ₹100, or ₹200 saved regularly is better than zero. The habit matters first.

Best ways to build an emergency fund:

- set auto-transfer on salary day

- save part of bonuses or gift money

- cut 2-3 unnecessary monthly expenses

- keep the money in a separate bank account

- do not connect it to frequent spending apps if you are impulsive

Image source: Public Domain Pictures

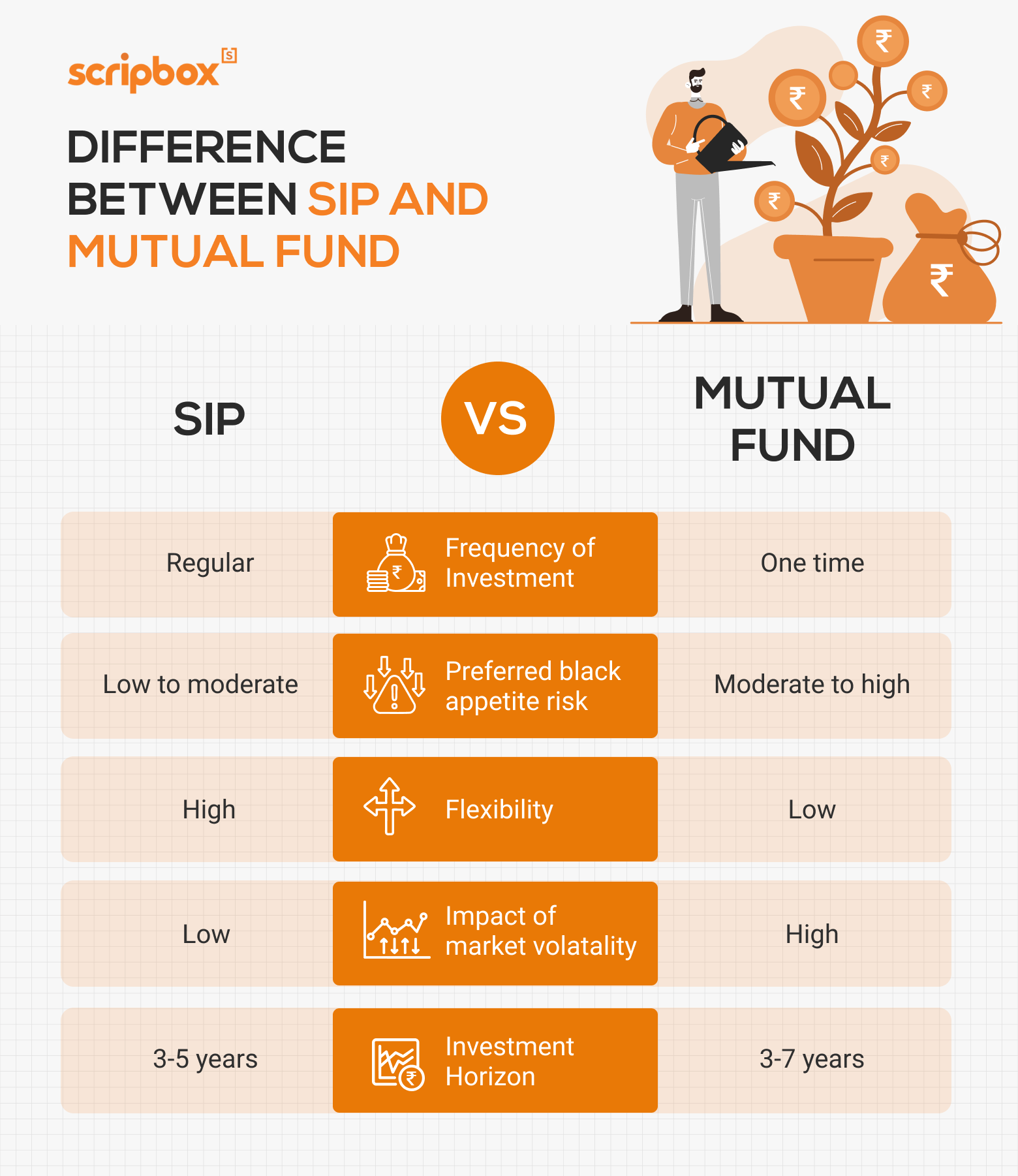

Step 4: Start Investing With Confidence, Not Confusion

Once you have basic control over spending and at least a starter emergency fund, you can begin investing. Many young people delay investing because they think they need a lot of money. That is not true. What matters most is starting early and staying consistent.

For beginners, one of the simplest ways to invest is through a systematic approach like SIPs in mutual funds, where small amounts are invested regularly over time. SEBI’s investor education material highlights that mutual funds offer professional management, diversification, transparency, convenience, and SIP options for regular investing [Source](https://investor.sebi.gov.in/understanding_mf.html).

That does not mean you should invest blindly. Before investing, ask:

- What is my goal?

- How long can I stay invested?

- Can I handle ups and downs?

- Am I investing after clearing high-interest debt?

For most young beginners, broad categories of goals look like this:

- Short-term goals: gadgets, travel, exam fees, emergency top-up

- Medium-term goals: higher education, vehicle, business fund

- Long-term goals: home down payment, wealth building, retirement

A smart beginner mindset is simple: first build discipline, then build wealth. Do not invest because a friend, influencer, or random reel told you to. Invest because your plan says it makes sense.

How Much Should a Young Adult Save and Invest Every Month?

There is no one perfect number, but a strong beginner approach is this:

- save something every month, even if small

- clear high-interest debt aggressively

- build emergency fund steadily

- start investments with an amount you can continue for years

Consistency beats intensity. A person who invests a modest amount every month for years often beats someone who starts late with bigger amounts.

Credit Card Rules Every Young Person Should Follow

Credit cards are not evil, but careless use can destroy your financial progress.

- Never spend on a credit card unless you already have the money to repay it.

- Always aim to pay the full bill, not just the minimum due.

- Do not use multiple cards unless you are highly disciplined.

- Do not lend your card to friends or relatives.

- Track due dates and turn on alerts.

- Avoid using credit cards for emotional spending.

If your current credit card balance is already stressing you out, stop new discretionary spending immediately and shift into payoff mode.

Money Habits That Can Make You Richer in the Long Run

Financial success is not usually built through one lucky investment. It is built through repeatable habits:

- track every rupee for 30 days

- pay yourself first on salary day

- avoid lifestyle inflation after every raise

- increase savings when income grows

- review goals every 3 months

- learn before investing

- keep your financial life simple

Simple habits look boring, but boring often wins in personal finance.

Financial Planning for Students, Freelancers, and First Jobbers

If you are still studying or your income is irregular, your financial plan will look a little different. Your first goal should be cash discipline, not complex investing.

For students

Learn budgeting, avoid unnecessary debt, and start a small savings habit.

For freelancers

Create an irregular income fund, save more during high-income months, and separate personal and work money.

For first job holders

Do not celebrate your first salary by locking yourself into long EMIs. Start with savings, emergency fund, and skill-building.

Your 90-Day Financial Reset Plan

Days 1-7

- write down total income

- list all expenses

- list every debt

- stop unnecessary subscriptions

Days 8-30

- create a simple monthly budget

- start a small emergency fund

- cut impulsive spending

- set up payment reminders

Days 31-60

- pay extra toward the highest-priority debt

- build a one-month spending buffer if possible

- discuss money openly with family if needed

Days 61-90

- review your progress

- increase savings by a small percentage

- begin a disciplined investment plan if debt is under control

- set 1-year and 3-year financial goals

Pro Tip: Do not wait for the perfect salary, perfect month, or perfect plan. Start with the money you have, improve gradually, and stay consistent.

How to Make Your Financial Plan Sustainable

The best financial plan is not the most advanced one. It is the one you can follow for years.

If your budget is too strict, you will quit. If your savings goals are unrealistic, you will lose motivation. If your investing plan is based on hype, you will eventually make emotional mistakes.

Keep it realistic. Keep it honest. Keep it simple.

Final Thoughts

If you are young and serious about changing your future, financial planning is one of the most powerful skills you can build. The goal is not to look rich. The goal is to become stable, free, and confident. First control spending. Then clear toxic debt. Then build emergency savings. Then invest with patience. This is how real wealth starts.

The biggest change in money does not come from one dramatic move. It comes from one good decision repeated every month.

Frequently Asked Questions

1. What is the first step in financial planning for young adults?

The first step is understanding your income, expenses, and debt clearly. Without that, no budget or investment plan will work.

2. Should I save first or pay debt first?

If your debt is high-interest, especially credit card debt, prioritize clearing it while also building a small emergency fund.

3. How much emergency fund should I have?

Start with a small target like ₹10,000 to ₹25,000, then slowly build toward 3 to 6 months of essential expenses.

4. Can I start investing with a small amount?

Yes. Starting small and staying consistent is often better than waiting for a large amount.

5. Are mutual funds good for beginners?

For many beginners, mutual funds can be a practical option because they offer diversification and professional management, but every person should invest according to their goals and risk profile [Source](https://investor.sebi.gov.in/understanding_mf.html).

6. Is credit card debt dangerous?

It can become dangerous very quickly if you do not clear the balance in full and keep spending beyond your repayment ability.

Disclaimer

This article is for educational purposes only and does not constitute personalized financial, legal, or investment advice. Always do your own research and consult a qualified professional before making major financial decisions.

Recommended Image Credits for This Article

Sources