Legal Limit: How Much Money Can You Send from USA to India?

How Much Money Can You Send to India Legally? A Complete Guide (2025)

A comprehensive guide to understanding legal limits, tax implications, and the best methods for sending money to India from abroad.

Understanding the legal framework for international money transfers to India

Introduction

In today's globalized world, sending money across borders has become a common necessity for millions of people. Whether you're an NRI (Non-Resident Indian) supporting family back home, investing in property, or funding a business venture, understanding the legal framework for international money transfers to India is crucial.

India, with its robust financial regulations and growing economy, has specific rules governing inward remittances. These regulations aim to balance the free flow of foreign exchange while preventing illegal activities such as money laundering and tax evasion.

This comprehensive guide covers everything you need to know about the legal limits, regulatory requirements, tax implications, and best practices for sending money to India. We'll also compare various money transfer services to help you make an informed decision based on your specific needs.

Key Takeaways

- There is technically no upper limit on how much money an NRI can send to India, but different regulations apply based on the purpose and amount.

- The Liberalized Remittance Scheme (LRS) allows Indian residents to receive up to $250,000 per financial year.

- Tax implications vary depending on the purpose of remittance, relationship between sender and receiver, and amount.

- Proper documentation and following compliance requirements are essential for seamless transfers.

- Choosing the right money transfer service can save you significant money on fees and exchange rates.

Legal Limits for Sending Money to India

Infographic showing tax implications on money transfers to India

Liberalized Remittance Scheme (LRS)

The Liberalized Remittance Scheme (LRS) is a framework introduced by the Reserve Bank of India (RBI) that governs inward remittances. Under this scheme:

- Resident Indians can receive up to $250,000 per financial year (April-March) without requiring specific permissions.

- This limit applies to the receiving party in India, not the sender abroad.

- The money can be used for various purposes including investments, education, medical expenses, and family maintenance.

Limits for Non-Resident Indians (NRIs)

For Non-Resident Indians sending money to India:

- There is technically no upper limit on how much money an NRI can send to India through banking channels.

- However, large transfers may require additional documentation and may be subject to closer scrutiny.

- Different rules may apply based on the purpose of the remittance (gifts, investments, property purchases, etc.).

Country-Specific Regulations (USA Example)

If you're sending money from the USA to India:

- The US has a "Gift Tax" policy where the first $14,000-$16,000 (amount varies by year) sent per person annually is tax-exempt.

- Any amount above the annual exclusion may be subject to gift tax, though this is typically only applied once the lifetime exemption ($12.92 million as of 2023) is exceeded.

- Transfers over $10,000 are automatically reported to the IRS through Currency Transaction Reports (CTRs).

Important Note

While there may not be strict limits on sending money to India, all transfers must comply with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations in both the sending and receiving countries. Large or unusual transactions may trigger additional verification steps.

Regulatory Framework

FEMA Regulations

The Foreign Exchange Management Act (FEMA) is the primary legislation governing all foreign exchange transactions in India. Key aspects of FEMA include:

- Classification of transactions as either capital or current account transactions.

- Guidelines for residents and non-residents on handling foreign exchange.

- Regulations to ensure that foreign exchange is used for legitimate purposes.

Evolution of money transfer systems and regulations

RBI Guidelines

The Reserve Bank of India (RBI) implements FEMA through various guidelines:

- The Money Transfer Service Scheme (MTSS) allows personal remittances of up to $2,500 per transaction, with a maximum of 30 transactions per calendar year per beneficiary.

- The Rupee Drawing Arrangement (RDA) method has no limit on receiving personal inward remittances, but business remittances are capped at INR 15 lakhs per transaction.

- All inward remittances must be routed through authorized banking channels.

Compliance Requirements

To comply with regulations, both senders and receivers must:

- Use only authorized banking channels for transfers.

- Provide proper documentation including purpose codes for the remittance.

- Report large transactions as required by law.

- Maintain records of remittances for potential audits.

- Ensure the transfer adheres to anti-money laundering (AML) regulations.

Recent Updates

The regulatory framework for international money transfers is periodically updated. As of 2025, the RBI has streamlined many processes to make remittances easier while maintaining necessary safeguards. Always check the latest regulations before making large transfers.

Tax Implications

Tax Considerations in the Sending Country (USA Example)

When sending money from the USA to India, consider these tax implications:

- Annual Gift Tax Exclusion: Up to $16,000 (2023 figure) per recipient per year is exempt from gift tax.

- Lifetime Gift Tax Exemption: Currently $12.92 million (2023), meaning most people will never pay gift tax.

- Reporting Requirements: Transfers over $10,000 are automatically reported to the IRS through Currency Transaction Reports (CTRs).

- FBAR Filing: US residents with foreign bank accounts totaling over $10,000 at any time during the year must file an FBAR (FinCEN Form 114).

Tax compliance considerations for international money transfers

Tax Considerations in India

For the recipient in India, tax implications depend largely on the nature of the remittance:

- Gifts from Relatives: Gifts received from relatives (as defined by the Income Tax Act) are completely tax-exempt, regardless of the amount.

- Gifts from Non-Relatives: Gifts exceeding ₹50,000 in a financial year from non-relatives are taxable in the hands of the recipient under "Income from Other Sources."

- NRE Account Transfers: Money in NRE accounts enjoys tax benefits in India, including tax-free interest income.

- NRO Account Transfers: Interest earned on NRO accounts is taxable in India.

- Business Remittances: Money sent for business purposes is subject to applicable business taxation rules.

Who Qualifies as a "Relative" Under Indian Tax Laws?

Under Section 56(2) of the Income Tax Act, "relatives" include:

- Spouse of the individual

- Brother or sister of the individual

- Brother or sister of the spouse of the individual

- Brother or sister of either of the parents of the individual

- Any lineal ascendant or descendant of the individual

- Any lineal ascendant or descendant of the spouse of the individual

- Spouse of any of the persons referred to above

Tax Optimization Tip

If you're sending substantial amounts to someone who qualifies as a relative under Indian tax law, there's no limit to how much you can send without the recipient incurring tax liability in India. For non-relatives, consider staggering transfers across financial years to minimize tax impact if the total exceeds ₹50,000.

Documentation Requirements

Essential Documents Needed

When sending money to India, the following documentation is typically required:

- For the Sender:

- Valid identification (passport, driver's license, etc.)

- Proof of address

- Source of funds documentation (for larger amounts)

- For the Recipient:

- Full name as it appears on their bank account

- Bank account number

- Bank's IFSC code (Indian Financial System Code)

- Bank's SWIFT/BIC code (for international transfers)

- Bank branch address

- Transaction Details:

- Purpose of remittance (with appropriate purpose code)

- Relationship with the recipient (for personal transfers)

- Declaration forms (varies by service provider and amount)

Additional Documentation for Large Transfers

For larger transfers (typically over $10,000 or equivalent), additional documentation may be required:

- Detailed explanation of the source of funds

- Supporting evidence for the purpose of transfer (e.g., property purchase agreement, education fee invoice)

- Bank statements or other financial records

- Tax returns or income verification

Purpose Codes for Remittance

When sending money to India, you must specify the purpose of the remittance using standardized codes. Common purpose codes include:

| Purpose | Code | Description |

|---|---|---|

| Family Maintenance | S0301 | Remittance for family maintenance and savings |

| Personal Gift | S0302 | Remittance towards personal gifts and donations |

| Investment in Property | S0005 | Investment in real estate |

| Education | S1107 | Education-related expenses |

| Medical Treatment | S1108 | Medical treatment costs |

| Business Investment | S0021 | Funding for business operations |

Documentation Warning

Inaccurate or incomplete documentation can lead to delayed transfers, additional fees, or even rejected transactions. Always ensure all your documents are current, accurate, and match the details provided for the transfer.

Comparison of Money Transfer Methods

Comparison of popular international money transfer services

Traditional Bank Transfers

Pros

Cons

Online Money Transfer Services

Pros

Cons

Pros

Cons

Pros

Cons

Cost Comparison for Sending $1,000 to India

Below is a typical cost comparison for sending $1,000 to India through different methods (as of early 2025, rates are approximate and subject to change):

| Service Provider | Transfer Fee | Exchange Rate Markup | Total Cost | Speed |

|---|---|---|---|---|

| Traditional Bank | $35-50 | 2-4% | $55-90 | 2-5 days |

| Wise | $8-10 | 0-0.5% | $8-15 | 1-2 days |

| Xoom | $5-8 | 1-3% | $15-38 | Minutes to 24 hours |

| Remitly | $0-4 | 1-2% | $10-24 | Economy: 3-5 days Express: Minutes |

| Western Union | $5-10 | 1-3% | $15-40 | Minutes to 2 days |

Money-Saving Tip

When comparing money transfer services, don't just look at the transfer fee—the exchange rate markup often costs you more than the stated fee. Use a service like Wise or similar platforms that offer transparent mid-market exchange rates to save significantly on larger transfers.

Best Practices and Tips

How to Minimize Fees

- Compare multiple service providers before each transfer—rates and fees change frequently.

- Transfer larger amounts less frequently rather than smaller amounts more often.

- Use bank transfers to fund your remittance instead of credit cards, which often incur additional fees.

- Look for promotional offers and first-time user bonuses.

- Consider setting up regular transfers to benefit from loyalty programs.

Security Considerations

- Only use regulated, authorized money transfer services.

- Verify recipient details meticulously to avoid transfer errors.

- Keep records of all transfers, including confirmation numbers and receipts.

- Be wary of unusually favorable exchange rates—if it seems too good to be true, it probably is.

- Use secure internet connections when making online transfers.

- Enable two-factor authentication when available.

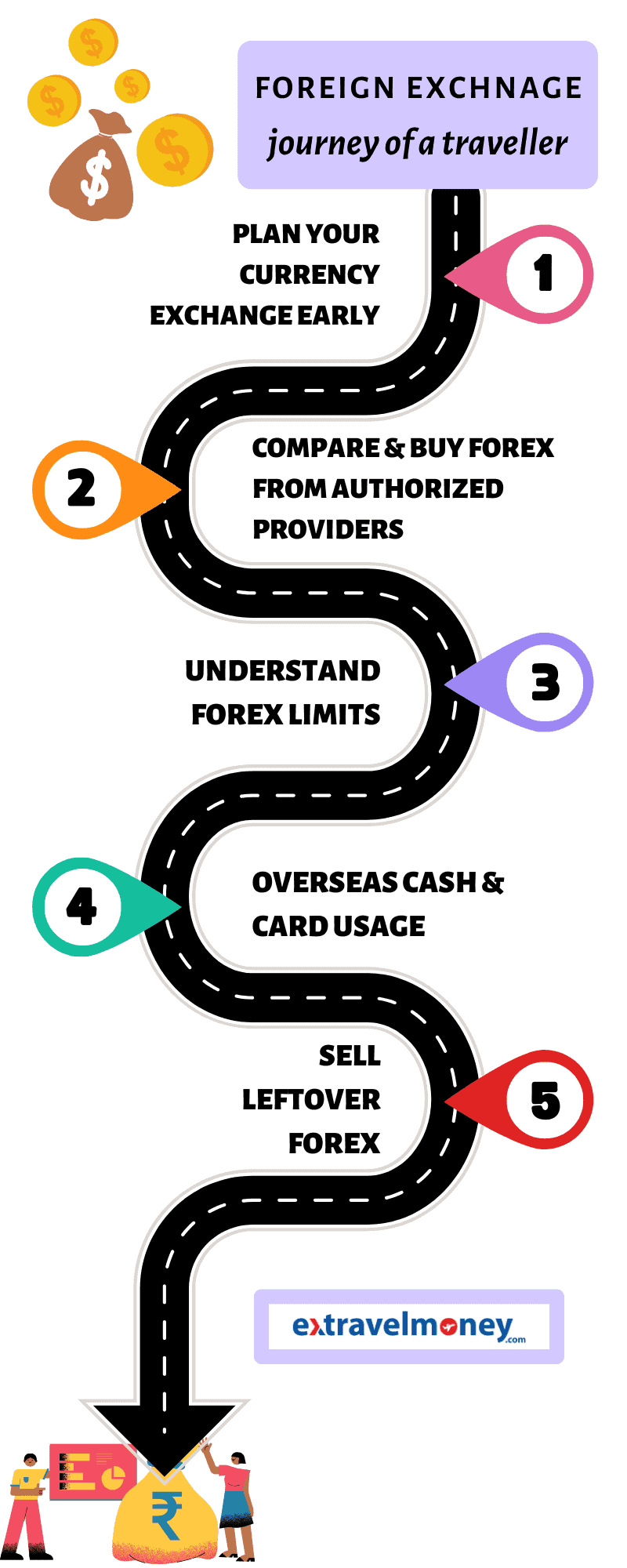

Guide to foreign currency exchange in India

Choosing the Right Service

The best money transfer service depends on your specific needs:

For large transfers ($5,000+)

Prioritize services with the best exchange rates over low fees. Traditional banks or specialized forex services like Wise, OFX, or XE might be best. These services often offer personalized assistance for large transfers.

For emergency transfers

When speed is critical, services like Western Union, MoneyGram, Xoom, or Remitly's express option can deliver funds within minutes, though at a higher cost.

For regular, smaller transfers

Online services like Wise, Remitly, or Xoom typically offer the best combination of reasonable fees, good exchange rates, and convenience for recurring transfers.

For recipients without bank accounts

Services offering cash pickup options like Western Union, MoneyGram, or Ria might be necessary, though they typically charge higher fees.

Exchange rates and fees fluctuate daily. Always compare current rates from multiple providers before making a transfer to ensure you're getting the best deal. Services like CompareRemit can help you find the best option for your specific transfer needs.

Frequently Asked Questions

Is there a limit on how much money I can send to India?

There is no upper limit on how much money an NRI can send to India through proper banking channels. However, resident Indians can receive up to $250,000 per financial year under the Liberalized Remittance Scheme (LRS). Large transfers may require additional documentation and verification.

Will the recipient have to pay tax on money I send to India?

It depends on the relationship and purpose. Gifts from relatives are completely tax-exempt regardless of amount. Gifts from non-relatives exceeding ₹50,000 in a financial year are taxable for the recipient under "Income from Other Sources." Money sent for specific purposes like education or business has different tax implications.

What documentation is required to send large amounts to India?

For large transfers, you typically need: valid identification, proof of source of funds, recipient's complete banking details (including IFSC and SWIFT codes), declaration of the purpose of remittance, and possibly additional documents depending on the amount and purpose (e.g., property purchase agreement for real estate investments).

Can I send money directly to an NRE or NRO account?

Yes, you can send money directly to both NRE (Non-Resident External) and NRO (Non-Resident Ordinary) accounts. NRE accounts are better for funds you may want to repatriate later, as they offer full repatriation benefits and tax-free interest. NRO accounts are typically used for income earned in India.

Do banks report large money transfers to tax authorities?

Yes, in most countries, banks and financial institutions are required to report large transfers. In the USA, for example, transfers exceeding $10,000 are automatically reported to the IRS through Currency Transaction Reports (CTRs). In India, banks report large transactions to the Financial Intelligence Unit (FIU-IND).

What's the fastest way to send money to India?

Services like Western Union, MoneyGram, Xoom, and Remitly offer "express" or "instant" transfers that can deliver funds within minutes to a few hours. These rapid services typically come with higher fees or less favorable exchange rates.

Can I send money to India without a bank account?

Yes, services like Western Union, MoneyGram, and Ria allow you to send money that can be picked up in cash at their agent locations in India. The recipient will need valid identification to collect the funds. However, for large amounts, bank transfers are recommended for better security and record-keeping.

Conclusion

Sending money to India legally involves understanding a complex web of regulations, tax implications, and service options. While there is technically no upper limit on how much money you can send to India through proper channels, compliance with regulations in both the sending and receiving countries is essential.

The key points to remember are:

- Indian residents can receive up to $250,000 per financial year under the LRS.

- Money sent to relatives in India is tax-exempt for the recipient, regardless of the amount.

- Gifts from non-relatives exceeding ₹50,000 are taxable for the recipient.

- Proper documentation and declaring the correct purpose of remittance are crucial.

- Comparing money transfer services can save you significant money, especially on larger transfers.

By understanding these regulations and following best practices, you can ensure that your money transfers to India are legal, cost-effective, and hassle-free. Whether you're supporting family, investing in property, or funding a business venture, careful planning and compliance with regulations will help you achieve your financial goals without unnecessary complications.

Post a Comment